Media Update: Netflix Subscription Fees, TikTok Returns, T-Mobile Acquisition

Linear news viewership jumped in early January, as some of President Trump’s cabinet nominees faced early Senate confirmation hearings and the Supreme Court ruled on TikTok’s bid to overturn the law requiring its divestiture. Despite the NFL entering the divisional round of the playoffs, sports and broadcast viewership has been down year-over-year.

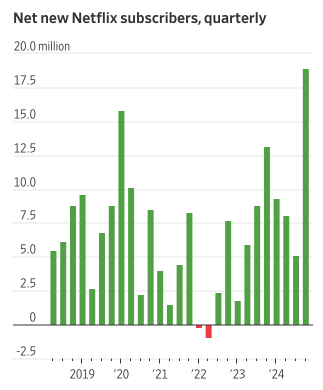

1. This week, Netflix announced it would increase monthly fees across its plans, with its cheapest ad-supported tier rising from $6.99 to $7.99 per month and the most expensive tier rising from $22.99 to $24.99. The increase comes amid strong subscriber growth for the platform, which gained nearly 19M subscribers in Q4 2024. Those impressive gains were fueled by a litany of premier live sports and entertainment content, including Jake Paul and Mike Tyson’s boxing match and two Christmas Day NFL games with a Beyonce halftime show.

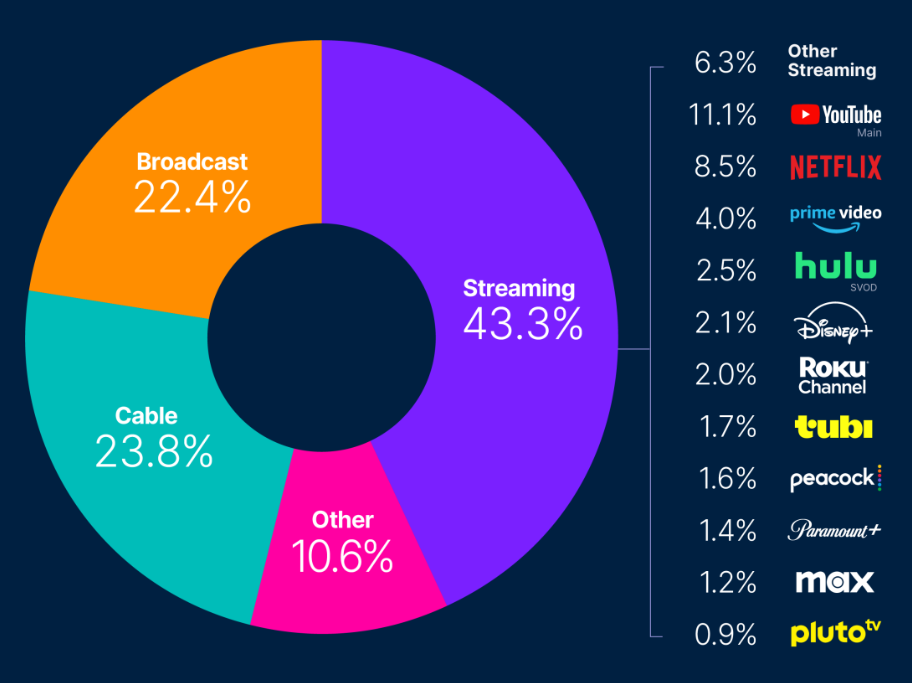

Viewership figures rose with the subscriber counts; while the streamer’s share of viewer attention had been relatively stagnant in recent months, December saw a significant boost as Netflix grew to 8.5% of viewer time, more than double the time spent with Prime Video and nearly a 1% jump month-over-month.

The subscription cost increases come at a relative low point for streaming CPMs. Netflix has been particularly impacted by these pressures, with its CPMs coming down by more than half since its initial launch, a trend exacerbated by the 2024 launch of ads on Prime Video. With revenue from advertisers pressured, Netflix is looking to support its financial picture with more revenue from customers, especially as more than half of new subscriptions in Q4 came from the ad-supported tier. That said, Netflix showed optimism for future ad sales, with co-CEO Greg Peters remarking, “We’ve doubled our ads revenue year-over-year last year. We expect to double it again this year, so that should give you a sense of the slope of monetization growth that we’re on.” Overall, Netflix’s announcement should be taken as another signal of the pressure all publishers – both large and small – are feeling in a hyper-fragmented, hyper-growth streaming landscape. For now, advertisers can take encouragement from a growing audience that is skewing more ad-supported, making Netflix an evermore appetizing investment opportunity. | WSJ, Nielsen

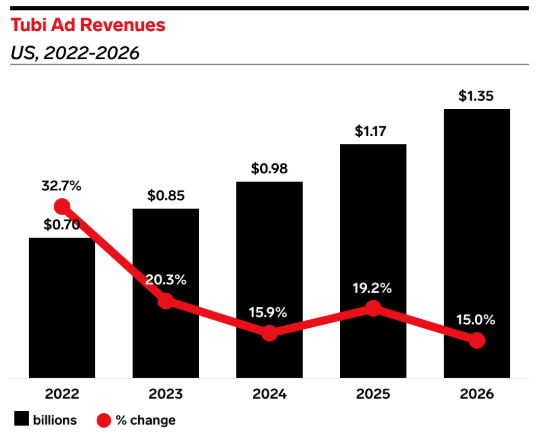

2. In a major coup for the free ad-supported television (FAST) streamers, Fox announced last week that it would stream Super Bowl LIX for free on Tubi. This marks the first time that the Super Bowl has been available free-of-charge on CTV, as access previously relied on having a paid subscription to a streamer or cable provider. Tubi, as well as other FAST networks like Roku and Pluto, has seen strong growth in the past year, with Tubi and Roku both outpacing Peacock, Paramount+, and Max in terms of viewership. Backed by this growth, Tubi’s ad revenues are expected to jump significantly this year, especially with Super Bowl LIX in support.

Fox scored another sports win this week, landing the rights to LIV golf. LIV tournaments will be aired on both linear and streaming platforms, which could help grow the tour, which saw weak ratings when it previously aired on the CW, despite several high-profile participants. Fox has clearly put an emphasis on its streaming sports offering, maintaining a focus even in the aftermath of the scrapped Venu project. As we’ve noted many times before, sports and live events remain one of streaming’s biggest opportunities for continued growth against linear, and Fox’s announcements – coupled with some of the big Netflix events we discussed above – make clear that the publishers are fully embracing this reality. | eMarketer, CNN

1. TikTok has had a whirlwind few days, starting with a brief shutdown of its U.S. operations on January 18th in response to a federal ban. By January 19th, operations resumed following ~15 hours of downtime and assurances from President Trump, culminating in an executive order on January 20th granting TikTok a 75-day grace period to remain operational. Despite being back online, TikTok and other ByteDance-owned apps remain unavailable in U.S. app stores, leaving critical software updates inaccessible, which could lead to eventual platform degradation. The timeline is precarious—TikTok must either secure a deal to divest U.S. operations or face enforcement actions when the extension expires on April 5th. For now, advertisers report a rebound in campaign activity, with more efficient CPMs and lower CPAs as platforms regain traction​

For advertisers, the uncertainty surrounding TikTok presents both opportunities and risks. On the positive side, current performance metrics are strong, but challenges remain as the app’s absence from stores prevents updates that could mitigate user experience issues over time. Advertisers should weigh the short-term gains of engaging with TikTok against the possibility of another shutdown. Diversification across other platforms is prudent, and brands should stay closely attuned to the latest developments. Additionally, any broader moves to regulate foreign-owned apps could have implications across the social media ecosystem, making adaptability a key strategy for 2025. | Forbes, BBC, New York Times

2. Bluesky is the latest platform to adopt a TikTok-inspired vertical video feed, aligning with the industry-wide pivot to immersive video content. This new feature allows users to swipe vertically through videos, tailored to their feed and community preferences. Unlike other platforms, Bluesky’s emphasis on decentralized control ensures that users dictate their experience, not corporate algorithms. This push aligns with the broader ethos of Bluesky and decentralized platforms, empowering users with more personalized, adaptable content feeds. Alongside Bluesky, the independent “Tik” app, built on the same AT Protocol, is positioning itself as another TikTok alternative. Tik users will even be able to integrate Bluesky content seamlessly, enabling cross-platform sharing without centralized oversight.

This move could prove timely, especially as uncertainty around TikTok’s ownership and future in the U.S. continues. For advertisers, while ads are still not available on either platform, this shift signals the growing appeal of decentralized networks, potentially fragmenting the social media landscape further. Brands should explore how to engage organically on emerging platforms like Bluesky to remain agile and prepared for a potential industry transformation toward decentralized social ecosystems. | SocialMediaToday

Mergers and acquisitions have been the theme so far this year. Harry has been covering some of the mergers this month in streaming, most notably the Disney and Fubo merger. Now, T-Mobile has entered the spotlight by acquiring Vistar, a digital out-of-home company.

With this deal, T-Mobile will acquire Vistar’s intelligent marketplace and technology to manage campaigns on over 1.1 million digital screens. This deal also adds to T-Mobile’s 2022 purchase of Octopus Interactive, a rideshare-focused ad startup that equips Uber and Lyft vehicles with interactive tablets, and signifies its ambition to be a major player in the out-of-home space.

The Vistar acquisition could unlock opportunities for out-of-home advertisers, paving the way for more sophisticated campaigns. While out-of-home remains a one-to-many medium, T-Mobile’s first-party data and location insights could help brands pinpoint their audience in real-world settings, allowing them to target more strategically and measure ad performance more effectively.

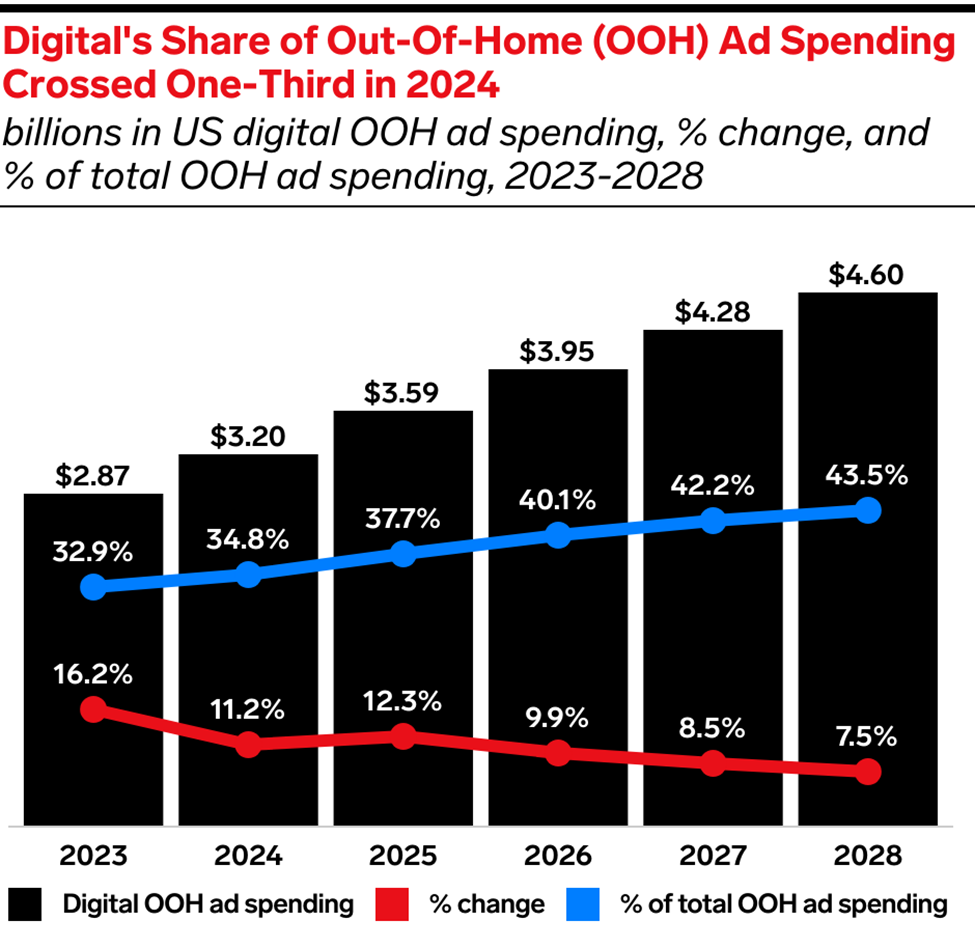

T-Mobile’s move into out-of-home advertising is timely. eMarketer projects that U.S. OOH ad spending will exceed $10 billion for the first time by 2027, 42% of which will come from digital formats. While we see this acquisition as one that could create new opportunities in the OOH space, we remain cautiously optimistic as the telecom sector’s track record with ad tech ventures warrants some skepticism. As the merger unfolds, it’s one we’ll be watching closely. | T-Mobile, AdExchanger, eMarketer

In a largely unexpected move, on Saturday January 18th, the same day that TikTok went temporarily dark in the US, Perplexity AI submitted a bid to ByteDance (TikTok’s parent company) proposing that Perplexity merge with TikTok U.S. Though any potential transaction would likely take months to complete, sources speculate Perplexity likely feels it has a chance with this bid since it’s proposing a merger, not an acquisition (ByteDance has already stated it wouldn’t fully sell TikTok).

If a merger were to happen, the move would be potentially transformative, allowing the quickly growing generative AI answer engine to tap into TikTok’s vast inventory of video content and bolster its answers with more visually compelling search results. Currently, Perplexity’s search results are largely text-based with limited visuals in most answers. This could be seen as a potential limitation compared to more widely used search engines (namely Google) where result pages have become increasingly visual and eye-catching in recent years. When videos are included in Perplexity’s answer results, the majority of those videos seem to be pulled from YouTube as opposed to other user-generated content sources, such as TikTok.Notably, Perplexity has been making other moves to integrate additional data sources into its tech stack. Back in mid-December, Perplexity announced its acquisition of Carbon, a retrieval engine that connects data sources to LLMs, making it possible to connect apps such as Google Docs directly to Perplexity’s answer engine. And earlier this week, Perplexity announced Sonar Pro API, its solution that enables real-time, web-wide research with citations to enhance generative search tools by providing more accurate, up-to-date answers. This development will improve online search by delivering more accurate, research-backed results in real time. These types of acquisitions and developments, in addition to the recent bid for a merger with TikTok U.S., suggest this still new-to-market competitor in the search space isn’t letting its foot off the gas any time soon. | CNBC, WSJ

Previously, we’ve highlighted Amazon’s ever-expanding presence in the advertising ecosystem. While Q4 2024 results are expected in early February, Amazon reported 19% year-over-year growth in ad revenue for Q3 2024, totaling $14.3 billion. This growth stems not only from its massive reach and loyal user base but also from strategic partnerships and cutting-edge ad tech infrastructure.

At CES 2025, Amazon unveiled its latest strategic move: the beta launch of Retail Ad Service. This platform aims to enable retailers to leverage Amazon’s technology for their own retail media networks (RMNs). With every brand holding customer emails and transaction histories eyeing RMNs as a revenue driver, this solution positions Amazon as the go-to partner for those seeking to enter this space. By offering a ready-to-deploy infrastructure, Amazon eliminates the challenges of building RMNs from the ground up, allowing retailers to focus on scaling and monetizing faster. While this may be viewed as a move to democratize access for brands to deploy RMNs, it is perhaps best viewed as Amazon’s attempt to increase its advertising footprint beyond its own ecosystem and across the open web. As RMNs continue to proliferate, Amazon’s strategy could redefine industry standards for customer engagement and monetization. It’s likely that Amazon envisions itself as the backbone of RMN technology, particularly as these networks consolidate to capture greater reach and advertiser attention. In an era of RMN expansion, Amazon seems well-positioned to shape the future of retail advertising. | CNBC, Amazon

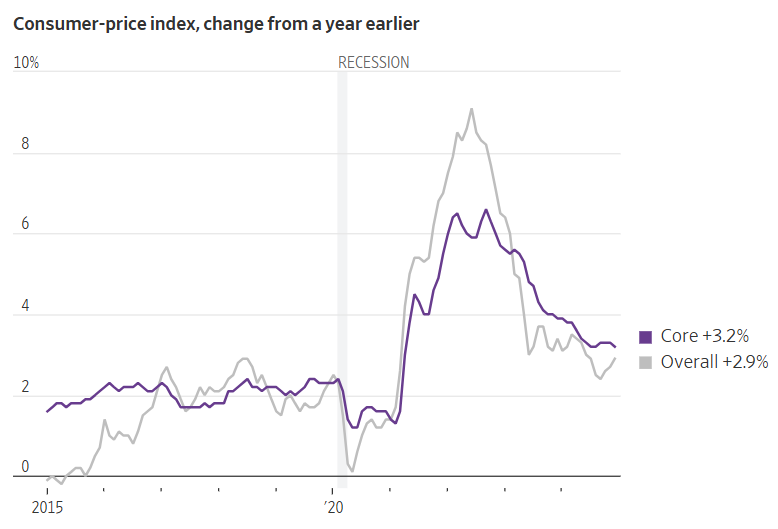

1. The third week of the new year brought a fresh inflation print, showing the CPI accelerated to 2.9% YoY in January, while “core” CPI declined to 3.2%. It is important to note that the Fed’s preferred gauge of inflation, the personal consumption expenditure (PCE) index, was considerably lower at 2.4% in its most recent reading in November.

Markets welcomed the news, with both equity and bond markets rallying; presumably, market participants’ inference is that the data will allow, or at least not prevent, the Fed from lowering interest rates throughout 2025. Futures markets currently imply about a 16% chance that the Fed does not cut rates at all this year.

The Fed has a complicated path ahead, however. From the perspective of a monetary policy maker aiming to restrain increases in the price level, one would hope for strong productivity growth and small budget deficits (or, as long as we’re dreaming, budget surpluses!). The new Trump administration appears to be intent on making the Fed’s job harder in this respect; we’ll refrain from opining on the wisdom of any of these policy proposals, but tariffs, tax cuts, and a crackdown on immigration all cut against at least one of these priorities. Even amid all this policy uncertainty, market participants see a high probability (per above) of interest rate reduction this year. | WSJ

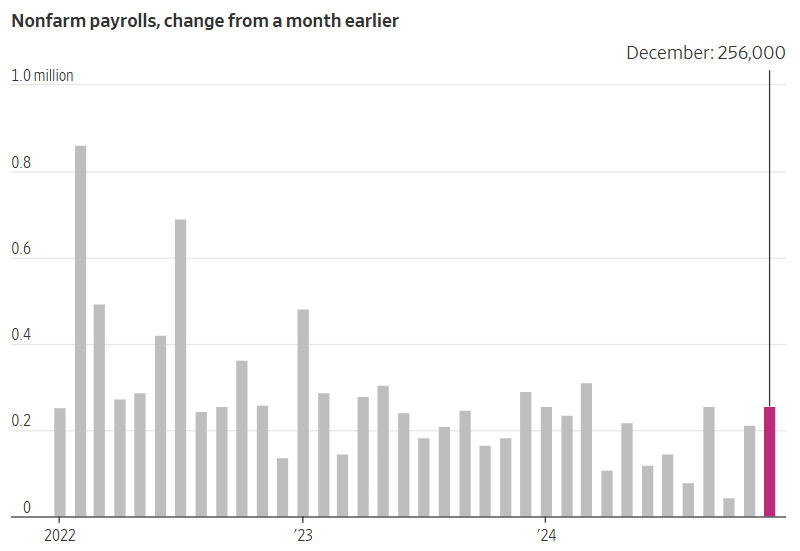

2. The week prior to the inflation report, we got a fresh jobs report that showed hiring blew past expectations in December, with employers adding over a quarter-million new jobs during the month. The strong hiring pushed down the unemployment rate slightly to 4.1%, higher than its historic lows during the post-COVID expansion but still extremely low by historical US standards.

The strong December numbers cap a terrific year for the US labor market. For the whole of 2024, American employers added 2.2 million jobs, more than double the number expected at the beginning of the year. Moreover, while 75% of new jobs in 2024 were added in just three sectors – healthcare, leisure & hospitality, and government, at least two of which are generally regarded as having low productivity – December’s additions were highly diversified across retail, professional and business services, information technology, and finance.

Perhaps the most encouraging data point from the jobs report was moderate nominal wage growth, which came in at +0.3% MoM, somewhat slower than the prior month. Nominal wage growth is regarded as the most reliable leading indicator of price inflation, so the Fed will regard this as a welcome data point. All signs from the labor market seem to be pointing toward the hoped-for soft landing; now inflation just needs to complete the final lap. | WSJ